The Total Capital Investment refers to the fixed costs that are associated with a process. This is calculated as the sum of the following cost items over all sections of a process:

3. Startup and Validation Cost

In addition, the Capital Investment Charged to This Project is determined. This corresponds to the fraction of Total Capital Investment which is considered in the economic analysis of a particular project. This is useful in situations of multi-product facilities, in which an entire section or certain equipment of a section may be utilized by multiple projects; for more details, see Capital Investment Charged to This Project.

Here is where you can find these figures:

● Both figures (Total Capital Investment and Capital Investment Charged to This Project) are shown in the Executive Summary Dialog: Summary Tab and in Sections 1 (Executive Summary) and 10 (Profitability Analysis) of the Economic Evaluation Report (EER).

● The Total Capital Investment is also shown in the Executive Summary Dialog: Capital Investment Tab.

● The individual cost items that contribute to the Total Capital Investment are shown in the Executive Summary Dialog: Capital Investment Tab and in Section 10 (Profitability Analysis) of the Economic Evaluation Report (EER).

Note that the Section 10 (Profitability Analysis) of the Economic Evaluation Report (EER) is generated only if the revenues of a project are positive.

The individual cost items that contribute to the Total Capital Investment are described in detail below.

The DFC refers to the fixed assets of an investment, such as plant and equipment. It is calculated at the process section level as the sum of direct, indirect and miscellaneous costs that are associated with a plant” s capital investment. The direct costs include cost elements that are directly related to an investment, such as the cost of equipment, process piping, instrumentation, buildings, facilities, etc. The indirect costs include costs that are indirectly related to an investment, such as the costs of engineering and construction. Additional costs such as the contractor’s fee and contingencies are included in miscellaneous costs.

By default, the DFC is estimated using cost correlations to estimate the purchase cost of all major process equipment and cost factors with respect to purchase cost to generate estimates for all other cost elements. The installation factors are equipment-specific, whereas all other factors are specified at the section level.

Here is where you can find DFC-related figures:

● The Equipment Purchase Cost and DFC are shown in the Executive Summary Dialog: Capital Investment Tab.

● The DFC is also shown in Section 10 (Profitability Analysis) of the Economic Evaluation Report (EER). Note that this section is generated only if the revenues of a project are positive.

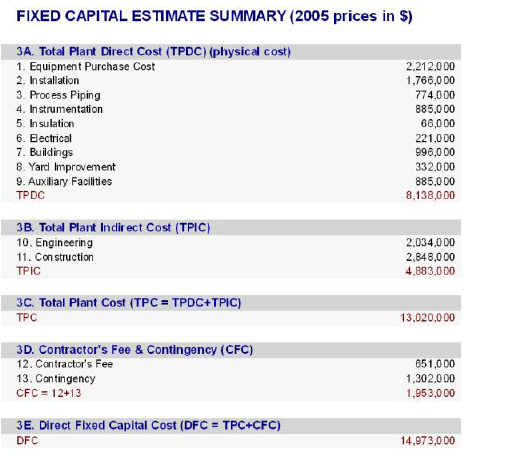

● The individual cost items that contribute to the DFC are shown in Section 3 (Fixed Capital Estimate Summary) of the Economic Evaluation Report (EER). An example is shown in The ‘Fixed Capital Estimate Summary’ section of the Economic Evaluation Report (EER)..

The ‘Fixed Capital Estimate Summary’ section of the Economic Evaluation Report (EER).

The individual cost items that contribute to the DFC and the available calculation options for the DFC are described in detail below.

The Total Plant Direct Cost (TPDC) is the sum of the following direct cost items:

● Equipment Purchase Cost (PC): this is the vendor's selling price of major equipment. It excludes items such as taxes, insurance, delivery and installation. It is also known as the free-on-board (FOB) cost. For a preliminary economic analysis, the purchase cost of equipment is typically estimated based on cost correlations. SuperPro Designer provides correlations for estimating the purchase cost of major listed (modeled) equipment. The user may also provide his/her own cost values or cost correlations for all listed (modeled) equipment; for more details on these options, see Purchase Cost of Listed Equipment below. In SuperPro Designer, PC is calculated at the section level. For each section, the user may also specify the purchase cost of unlisted (overlooked) equipment as a factor of the section’s PC. Generally, a section’s PC will be the sum of the purchase costs of listed and unlisted equipment for that section.

● Installation Cost: this cost item refers to the in-place construction of equipment at the new plant site and includes the cost of foundations, slabs, supports, and local equipment services. For a preliminary economic analysis, the installation cost of listed (modeled) equipment can be estimated by multiplying the corresponding purchase cost by a suitable factor; for more details, see Installation Cost of Listed equipment. In SuperPro Designer, the installation cost is calculated at the section level. For each section, the user may also specify the installation cost of unlisted (overlooked) equipment as a factor of the corresponding purchase cost of unlisted equipment for that section. Generally, a section’s installation cost will be the sum of the installation costs of listed and unlisted equipment for that section.

● Process Piping Cost: this cost item incorporates the cost of process fluid piping that connects the equipment, as well as connections to the main utility headers and vents. Included are valves, piping supports, insulation, and other items associated with equipment piping. For a preliminary economic analysis, this cost is typically estimated by multiplying PC by a suitable factor. In SuperPro Designer, this cost is calculated at the section level as a factor of the section’s PC.

● Instrumentation Cost: this cost item includes the costs of transmitters and controllers (with all required wiring and tubing for installation), field and control room terminal panels, alarms and enunciators, indicating instruments both in the field and in the control room, on-stream analyzers, control computers and local data-processing units, and control room display graphics. For a preliminary economic analysis, this cost is typically estimated by multiplying PC by a suitable factor. In SuperPro Designer, this cost is calculated at the section level as a factor of the section’s PC.

● Insulation Cost: this cost item includes the cost of insulation and painting, which is usually included in the cost of installation and piping. In low temperature plants, however, insulation cost can become unusually high. An insulation surcharge is recommended for such plants. For a preliminary economic analysis, this cost is typically estimated by multiplying PC by a suitable factor. In SuperPro Designer, this cost is calculated at the section level as a factor of the section’s PC.

● Electrical Cost: this cost item refers to the cost of electrical facilities. These includes battery limits substations and transmission lines, motor switch gear and control centers, emergency power supplies, wiring and conduit, bus bars, and area lighting. Separate equipment estimation is required for electrolytic installations. For a preliminary economic analysis, this cost is typically estimated by multiplying PC by a suitable factor. In SuperPro Designer, this cost is calculated at the section level as a factor of the section’s PC.

● Buildings Cost: this cost item includes the cost of process towers, subsidiary concrete slabs, stairways and catwalks (not equipment-specific), control rooms and other battery limits buildings (e.g., change rooms, cafeteria, furnished offices, warehouses, etc.). It also incorporates the costs for non-electric building services as well as for a variety of safety-related items. For a preliminary economic analysis, this cost is typically estimated by multiplying PC by a suitable factor. In SuperPro Designer, this cost is calculated at the section level as a factor of the section’s PC.

● Yard Improvement Cost: this cost item refers to the costs of excavation, site grading, roads, fences, railroad spur lines, fire hydrants, parking spaces, and others. For a preliminary economic analysis, this cost is typically estimated by multiplying PC by a suitable factor. In SuperPro Designer, this cost is calculated at the section level as a factor of the section’s PC.

● Auxiliary Facilities Cost: this cost item includes the cost of satellite process-oriented service facilities that are vital to the proper operation of the battery limits plant. An example of an auxiliary facility is a steam plant. For a preliminary economic analysis, this cost is typically estimated by multiplying PC by a suitable factor. In SuperPro Designer, this cost is calculated at the section level as a factor of the section’s PC.

The Total Plant Indirect Cost (TPIC) is the sum of the following indirect cost items:

● Engineering: this cost item includes the preparation of design books that document the whole process (e.g., the design of equipment, specification sheets for equipment, instruments, auxiliaries, etc., the design of control logic and computer software, the preparation of drawings) and other engineering-related costs. For a preliminary economic analysis, this cost is typically estimated by multiplying TPDC by a suitable factor. In SuperPro Designer, this cost is calculated at the section level as a factor of the section’s total direct cost.

● Construction: this cost item includes the costs associated with the organization of the total construction effort. They do not include the cost of construction labor. This is incorporated in direct cost items that involve construction. For a preliminary economic analysis, this cost is typically estimated by multiplying TPDC by a suitable factor. In SuperPro Designer, this cost is calculated at the section level as a factor of the section’s total direct cost.

The sum of TPDC and TPIC is denoted as Total Plant Cost (TPC).

The following additional costs are also considered:

● Contractor's Fee: this is the contractor's profit. It should be added even if a corporation does its own construction, because the construction division is expected to show a profit. For a preliminary economic analysis, this cost is typically estimated by multiplying TPC by a suitable factor. In SuperPro Designer, this cost is calculated at the section level as a factor of the section’s total direct and indirect costs.

● Contingency: the more speculative a process is, the more likely it is that key elements have been overlooked during the project's early stages. This cost attempts to compensate for missing elements. However, even advanced-stage estimates will include a contingency to account for unexpected problems during construction, such as strikes, delays, and unusually high price fluctuations. For a preliminary economic analysis, this cost is typically estimated by multiplying TPC by a suitable factor. In SuperPro Designer, this cost is calculated at the section level as a factor of the section’s total direct and indirect costs.

Based on the above definitions, the total DFC of an investment is calculated as the sum of TPC and CFC.

In SuperPro Designer, the DFC is estimated at the section level. Different options and parameters can be specified through a section’s Capital Investment Dialog: DFC Tab. To access the ‘Capital Investment’ dialog for a process section, first select the desired section in the ‘Section Name’ drop-down list box that is available on the ‘Section’ toolbar. Then, do one of the following:

● click Section Capital Cost Adjustments ( ) on the same toolbar, or

) on the same toolbar, or

● click Process Options } Section: <section name> } Capital Cost Adjustments on the Edit menu, or

● right-click on the flowsheet to bring up its context menu and click Section: <section name> } Capital Cost Adjustments.

Note that the term in brackets represents the name of the selected section. The DFC of a section can be either:

● set by user, or

● estimated by multiplying the section’s PC by a suitable ‘composite’ PC factor, or

● estimated as the sum of direct, indirect and other costs based on a distributed set of PC factors for the individual cost elements that contribute to these costs.

By default, a section’s DFC is estimated based on the third option. If the second or the third option is selected, the section’s PC must be first estimated. This is calculated as the sum of the total purchase costs of listed and unlisted equipment for that section. The total purchase cost of listed equipment for that section is calculated as the sum of individual purchase costs of all equipment present in that section. By default, the purchase cost of listed equipment is calculated using built-in cost correlations; for more details, see Purchase Cost of Listed Equipment. The total purchase cost of unlisted equipment for that section is specified as factor of the section’s PC.

If the DFC is estimated based on the third option, then additional cost items that contribute to the DFC are estimated. Similarly to the section’s PC, the section’s installation cost is calculated as the sum of total installation costs of listed and unlisted equipment for that section. The total installation cost of listed equipment for that section is calculated as the sum of individual installation costs of all equipment present in that section. The installation cost of listed equipment is specified as a factor of the equipment’s purchase cost; for more details, see Installation Cost of Listed equipment. The total installation cost of unlisted equipment for that section is specified as factor of the total purchase cost of unlisted equipment for that section. Additional cost items that contribute to the section’s DFC are specified as factors of the section’s PC.

|

|

SuperPro Designer uses a default set of PC factors that primarily applies to relatively large chemical and biochemical plants. These may be substantially off for small plants that produce high added value products, or for very large plants that produce commodity products. In these cases, appropriate PC factors must be specified by the user. |

|

|

You may choose to use site data for the PC factors. You can store distinct sets of economic factors behind model database sites and allocate the site with the most appropriate factors to relevant sections within your recipes; for more details, see Sites & Resources Databank. Alternatively, you may save the economic factors of different types of plants into different files and use those files as starting points (like templates) whenever you wish to analyze a new process with similar economic characteristics. |

Below, the calculation of the purchase and installation costs of listed equipment are described in detail.

The total purchase cost of a section’s listed (modeled) equipment is calculated as the sum of the purchase costs of all equipment resources of that section.

An equipment resource may represent multiple equipment units. It may include:

● a number of units (N) that are operated in parallel (i.e., simultaneously)

● extra sets of parallel units (M) that are operated in staggered mode (i.e., out of phase)

● a number of standby units (K)

Consequently, an equipment may represent a total of N(1+M)+K units. These values are specified through different tabs of the equipment’s simulation data dialog:

● The number of parallel units and the extra sets of staggered units are specified through the Equipment Data Dialog: Equipment tab.

● The number of standby units is specified through the Equipment Data Dialog: Adjustments Tab.

Note that in equipment ‘Design Mode’, the number of units that are operated in parallel is calculated as part of the simulation; for more details, see Main Equipment. To access the simulation data dialog of a host equipment, right-click on a unit procedure to bring up its context menu and select Equipment Data.

The purchase cost of an equipment resource will be equal to the corresponding purchase cost of a single unit of that type times the total number of units that it represents. For batch processes, only a fraction of that cost will be charged to each section. This is calculated as the fraction of total batch time that the equipment is in use by procedures contained in that section. This time factor is calculated by the program as part of the simulation.

Different specification options are available for the purchase cost of a single unit. These can be found in the Equipment Data Dialog: Purchase Cost Tab. The purchase cost of a single unit can be either:

a) set by the user, or

b) estimated based on a built-in model, or

c) estimated based on a user-defined model.

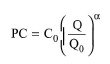

By default, the purchase cost of equipment is estimated based on built-in cost correlations according to the second option. SuperPro Designer provides correlations for estimating the purchase cost of all major listed equipment. If the third option is selected, custom cost correlations can be specified based on the following power law:

|

|

eq. (9.1) |

where:

● C0 is the base cost,

● Q0 is the base capacity, and

● α is the exponent of the power law.

You may break the whole capacity range into any number of intervals and specify a set of power law data for each interval. To account for the time value of money, you must also specify the reference year for which the cost is valid. If the purchase cost is set by user, you may also specify a reference year or let the cost be fixed (independent of the year of the analysis); for more details, see Purchase Cost.

The purchase cost in the year of analysis is calculated based on built-in values of the Chemical Engineering Cost Index for the reference year and the year of analysis. For years for which the Chemical Engineering Cost Index is not available, an inflation rate is used. The year of analysis and the inflation rate can be specified through the Economic Evaluation Parameters Dialog: Time Valuation Tab. To display the ‘Economic Evaluation Parameters for Entire Project’ dialog, do one of the following:

● click Process Options } Economic Evaluation Parameters on the Edit menu, or

● right-click on the flowsheet to bring up its context menu and click Economic Evaluation Parameters.

By default, the year of analysis for a new project is the present year and the inflation rate is 4%.

The number of units that are operated in parallel, the number of standby unit, the number of staggered units, the unit cost and the total cost of all equipment present in the process are listed in Section 2 (Major Equipment Specification and FOB Cost) of a project’s EER.

The total installation cost of a section’s listed (modeled) equipment is calculated as the sum of the installation costs of all equipment resources of that section. For batch processes, only a fraction of that cost will be charged to each section. This is calculated as the fraction of total batch time that the equipment is in use by procedures contained in that section. This time factor is calculated by the program as part of the simulation.

The installation cost of an equipment resource is specified as a factor of its purchase cost. SuperPro Designer provides default installation factors for all major listed equipment. The installation factor of an equipment resource can be viewed or edited through the Equipment Data Dialog: Adjustments Tab.

The working capital represents tied-up funds required to operate the business. It includes the investment in raw materials, consumables, etc. In SuperPro Designer, the working capital is specified at the section level. For each section, this can be either:

● set by the user, or

● estimated as the sum of major operational costs covered for a certain operating period; these include the costs for labor, raw materials, utilities (i.e., heating/cooling agents and power), waste treatment, and miscellaneous costs.

If the second option is selected, the user specifies the number of days that labor, raw materials, utilities and waste treatment costs are covered. The cost per section of each of the above items is calculated by multiplying the specified number of days by the corresponding daily cost of that item; for more details on the unit costs of the above cost items, see Operating Cost. In addition, the user may specify an amount of money that is attributed to miscellaneous costs. The working capital of a section is calculated as the sum of all the above cost items.

The specification options for the working capital of a section can be edited through the Capital Investment Dialog: Misc Tab.

The startup and validation cost includes pre-opening, one-time expenditures incurred to prepare a new plant for operation. In SuperPro Designer, the startup and validation cost is specified at the section level. For each section, this can be either:

● set by the user, or

● estimated as a percentage of DFC.

|

|

You may choose to use site data for the percentage of DFC that corresponds to the startup and validation cost of a section. You can store distinct sets of these factors behind model database sites and allocate the site with the most appropriate factors to relevant sections within your recipes; for more details, see Sites & Resources Databank. |

|

|

The startup and validation cost may optionally be depreciated; for more details, see Depreciation. |

The specification options for the startup and validation cost of a section can be edited through the Capital Investment Dialog: Misc Tab.

The up-front R&D cost accounts for the cost of research & development required before a product is manufactured. In SuperPro Designer, this is specified at the section level through the Capital Investment Dialog: Misc Tab.

The up-front royalties account for the payments made for use of assets, resources, patents, etc. prior to the initiation of a project. In SuperPro Designer, this cost is specified at the section level through the Capital Investment Dialog: Misc Tab.

For each section, you can modify the fraction of the DFC that is assigned to this project. This is useful in situations of multi-product facilities, in which an entire section or certain equipment of a section may be utilized by multiple projects. This cost allocation can be made either on a section-wide basis or on a equipment-by-equipment basis. In the latter case, the user specifies the fraction of an equipment’s purchase cost in that section which is assigned to this project. This information can be specified through the Capital Investment Dialog: Cost Alloc Tab.

|

|

If the DFC of a section is set by user, then only the section-wide cost allocation option will be available for that section. |

The Capital Investment Charged to This Project is determined based on the cost allocation specifications for each section. It is calculated similarly to the Total Capital Investment except that it accounts only for the fraction of DFC that is assigned to this project. Its value is listed in the Executive Summary Dialog: Summary Tab and also in Sections 1 (Executive Summary) and 10 (Profitability Analysis) of the Economic Evaluation Report (EER). Note that the latter section is only available if the revenues of a project are positive.